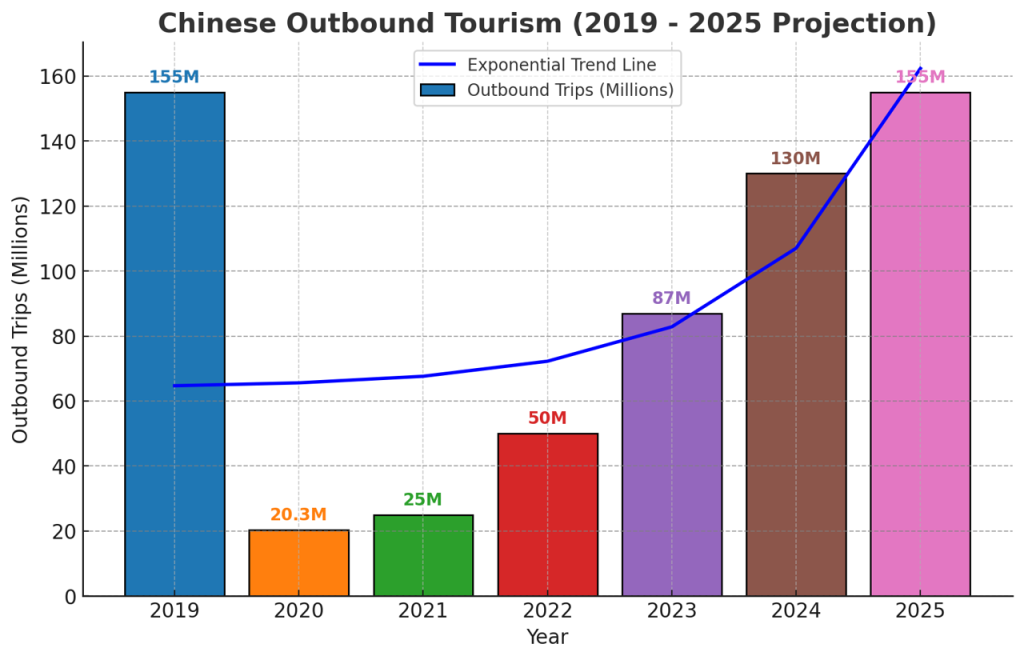

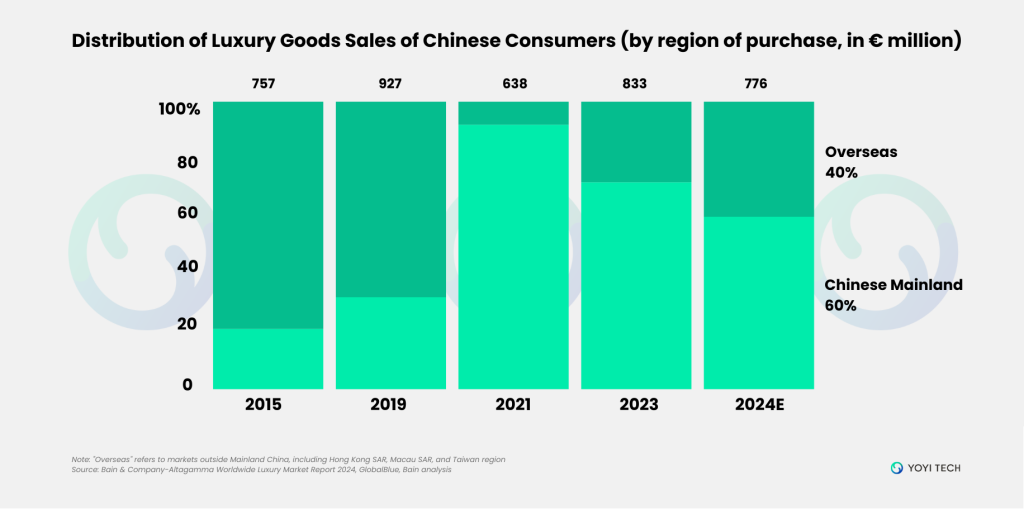

The Chinese luxury market remains a cornerstone of global growth, projected to capture 40% of worldwide luxury spending by 2025 (The Chinese luxury consumer, McKinsey). Post-pandemic recovery trends indicate a resurgence in overseas consumption, with 60% of purchases occurring domestically and 40% abroad—primarily in Europe and Asia-Pacific (Bain & Company-Altagamma Worldwide Luxury Market Report 2024). Despite this, China’s domestic market and its evolving consumer preferences demand strategic prioritization for global brands seeking sustained growth.

01 Key Overseas Destinations

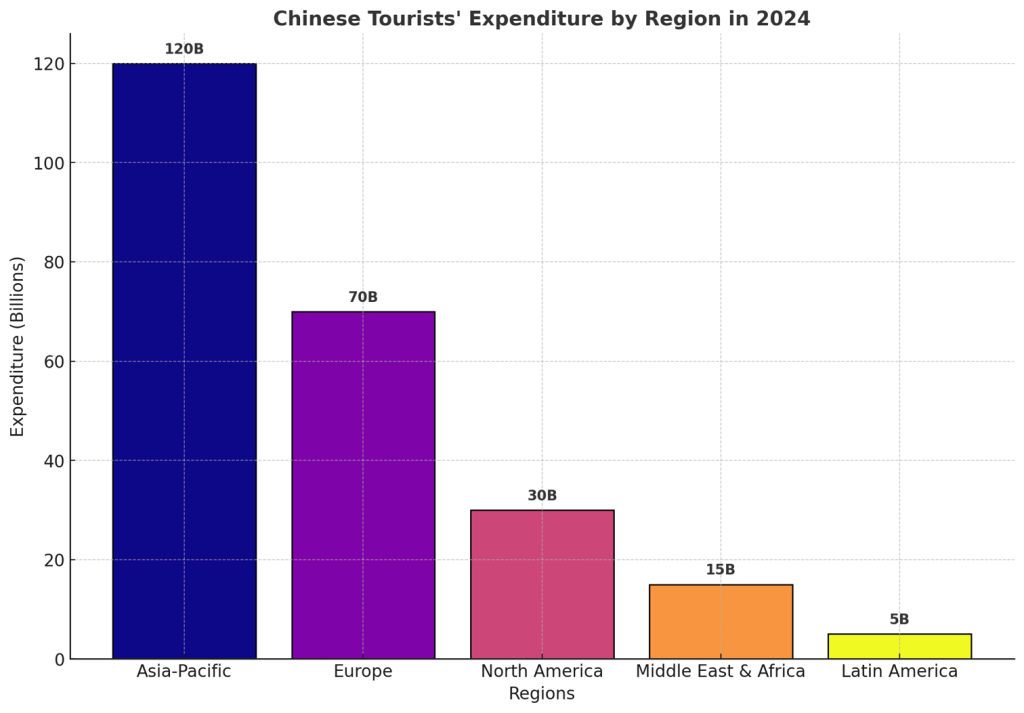

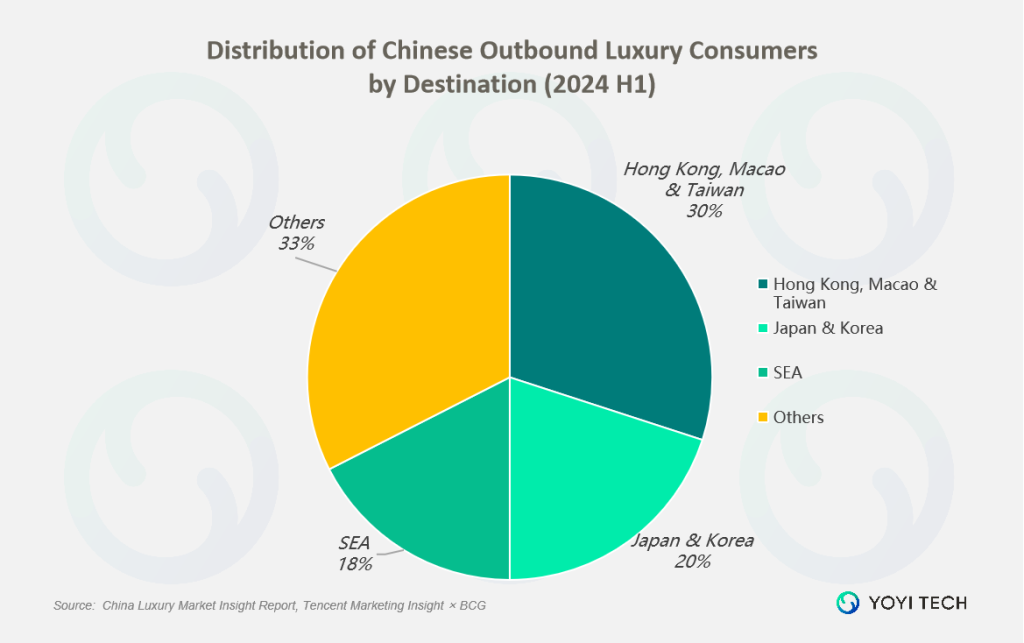

According to China Luxury Market Insight Report, published by Tencent Marketing Insight & BCG, Asia dominates as the primary destination for outbound luxury shopping, with Greater China (Hong Kong, Macao, Taiwan) accounting for 30% of purchases. Japan and South Korea follow at 20%, while Southeast Asia captures 18%.

02 Shopping Channels and Travel Integration Among Overseas Chinese Luxury Consumers

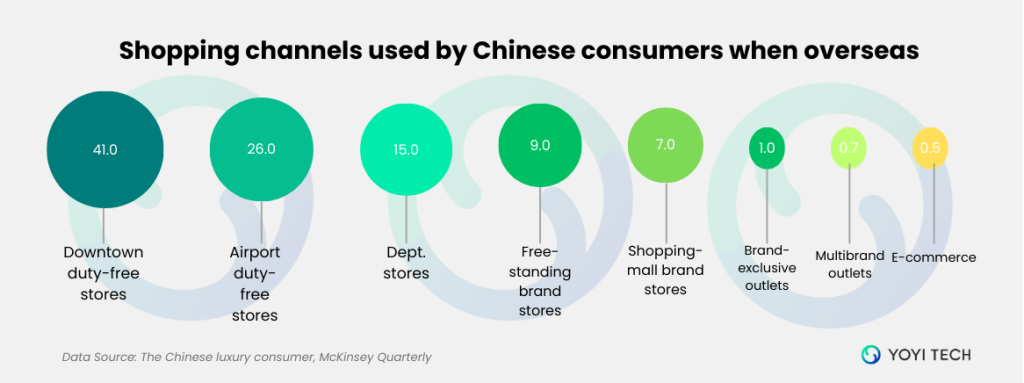

Chinese consumers exhibit a pronounced preference for duty-free channels when purchasing luxury goods abroad, with downtown duty-free stores (41%) and airport duty-free outlets (26%) emerging as the top choices (The Chinese Luxury Consumer, McKinsey Quarterly). This trend underscores the centrality of tax-free savings in purchasing decisions, particularly among price-sensitive yet high-spending cohorts. Beyond duty-free, consumers also frequent department stores, free-standing brand boutiques, and shopping-mall brand stores, though these channels remain secondary to the dominance of duty-free retail.

Notably, overseas luxury shopping is rarely isolated; it is often seamlessly integrated into premium travel experiences. Consumers prioritize curated itineraries that pair luxury purchases with high-end hospitality, gourmet dining, and cultural engagements, reflecting a holistic approach to luxury consumption. For brands, aligning with duty-free retailers in key travel hubs—such as airports and urban luxury districts—is critical to capturing this dual demand for exclusivity and experiential value.

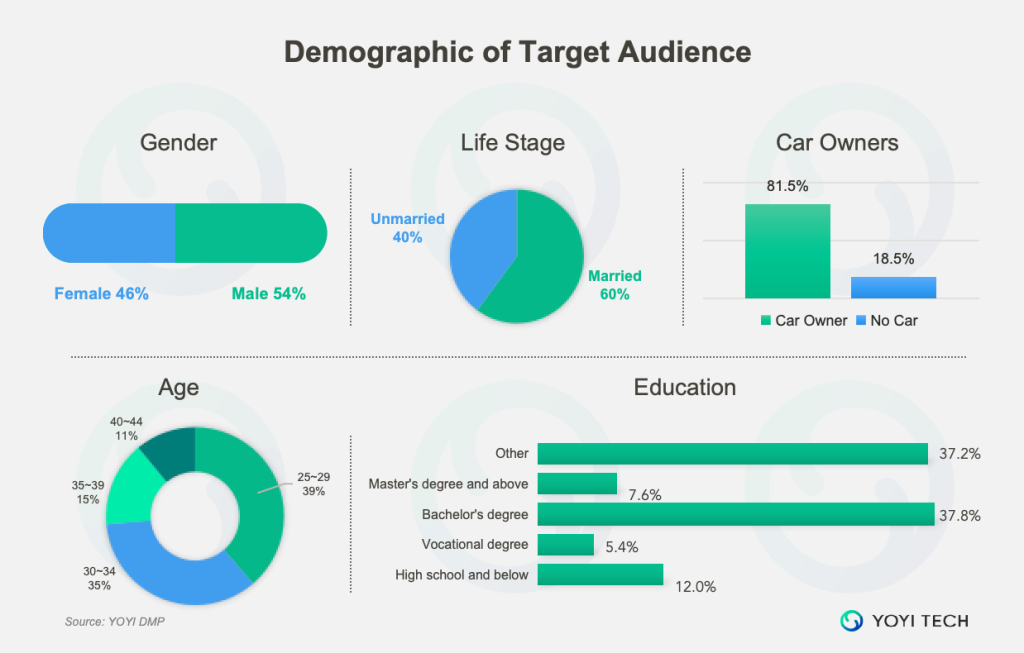

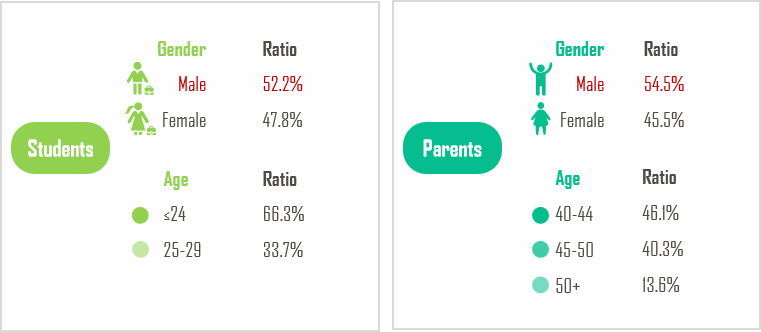

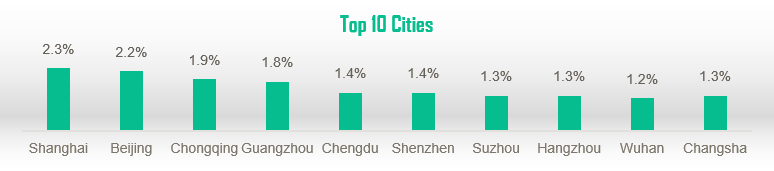

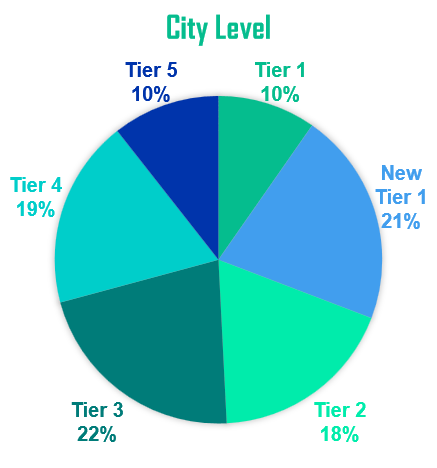

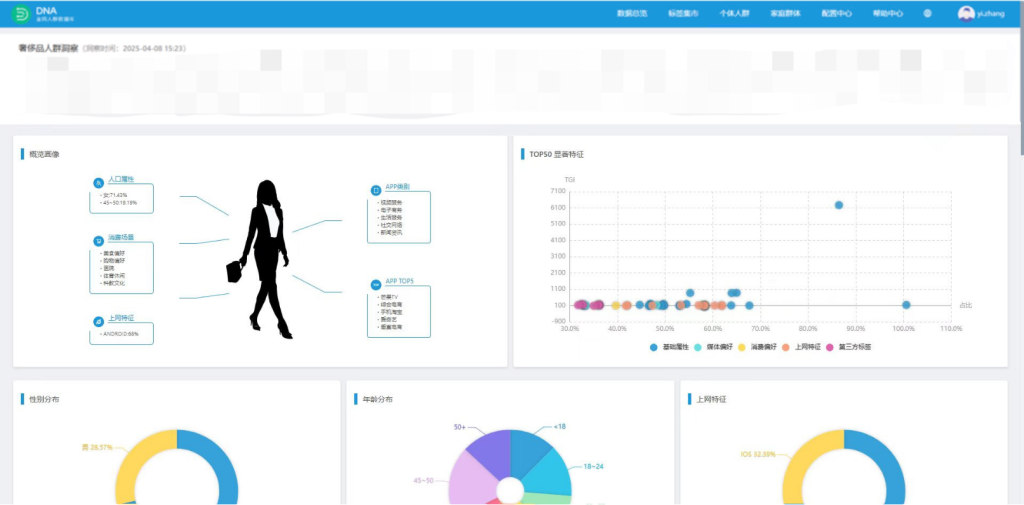

03 Consumer Demographics: Profiling the Luxury Cohort via YOYI DMP

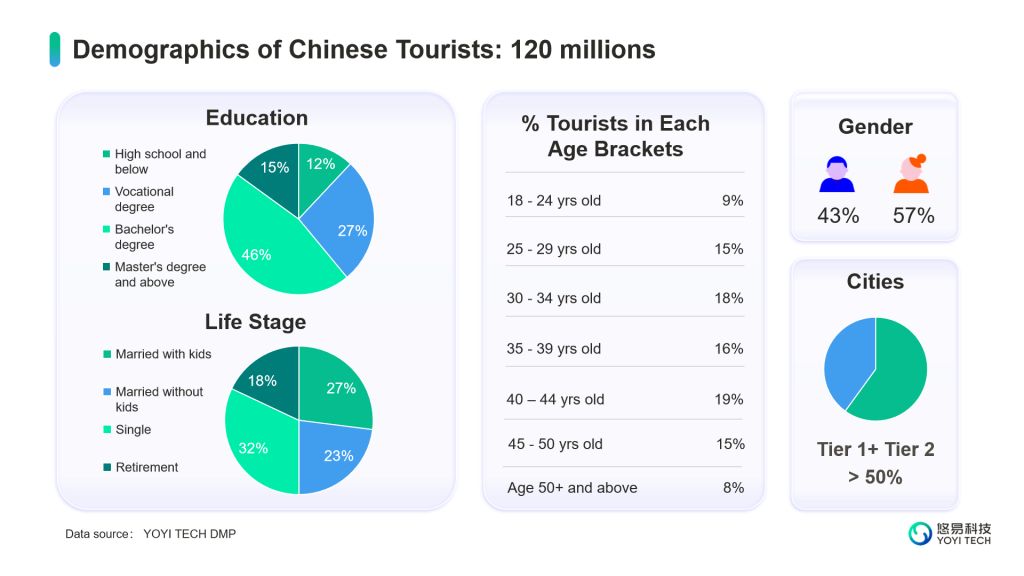

The core luxury demographic skews heavily female (70%), with nearly 20% aged 45–50. Geographically, 45% reside in Tier-1 cities such as Beijing, Shanghai, and Guangzhou, or emerging hubs like Chongqing, Chengdu, and Shenzhen. This cohort is characterized by high disposable income (90% car ownership), a significant proportion of unmarried individuals (57%), and a preference for integrated consumption scenarios—spanning gourmet dining, shopping, wellness, and sports.

04 Digital Engagement: The WeChat Ecosystem Imperative

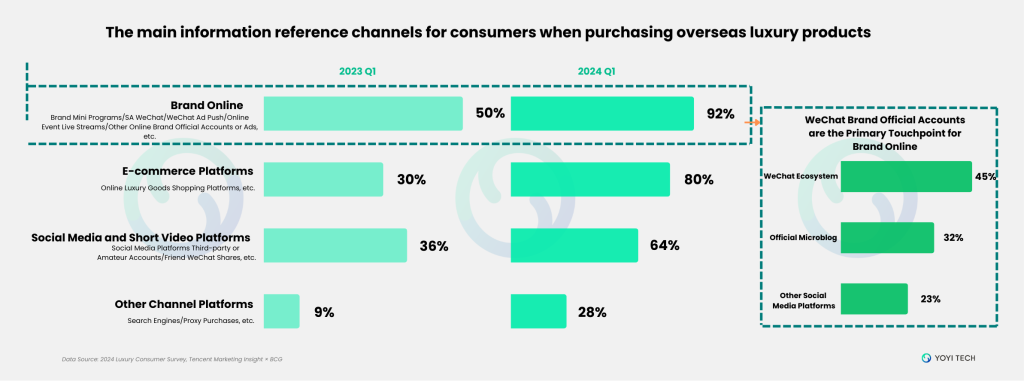

WeChat’s ecosystem has solidified its position as the central hub for Chinese consumers researching overseas luxury purchases. In Q1 2024, 92% of buyers relied on official brand channels—Mini-programs, live streams, official accounts, and websites—to inform their purchasing decisions (2024 Luxury Consumer Survey, Tencent Marketing Insight and BCG). Within this landscape, WeChat alone captures 45% of consumer attention, dwarfing other social media platforms (23%), underscoring its unparalleled influence in shaping buyer behavior.

Luxury brands leverage WeChat’s Official Accounts (OA) as a gateway to deepen digital engagement. According to Digital Luxury Group, 88% of brands strategically link their OAs to Mini-programs, embedding direct access points in OA menus, articles, and welcome journeys. This integration creates a seamless user experience, guiding consumers from brand content to transactional interfaces—such as product catalogs or exclusive pre-orders—within a single ecosystem.

Beyond digital interaction, WeChat Mini-programs serve as a bridge to physical retail. A robust 86% of luxury brands deploy Mini-program-based store locators, enabling consumers to identify nearby boutiques effortlessly. This feature, combined with inventory-checking tools, drives tangible foot traffic: 37% of brands utilizing store reservation services via Mini-programs. By integrating functionalities like associate-led consultations via WeCom, brands further personalize the path to purchase, merging online convenience with offline exclusivity.

WeChat’s dual role—as both an information powerhouse and an omnichannel facilitator—cements its indispensability for luxury brands targeting Chinese consumers. With over 1.3 billion active users, the platform not only offers unparalleled reach but also provides rich advertising formats embedded in Moments, Official Accounts (OA), Channels, Search, and more, enabling brands to engage audiences through hyper-targeted campaigns. By prioritizing mini-program development, store integration, and leveraging these dynamic ad touchpoints, brands can harness WeChat’s ecosystem to convert digital engagement into offline loyalty, ensuring alignment with the preferences of a sophisticated, tech-driven consumer base.

For actionable insights into the nuanced behaviors of Chinese luxury consumers and proven methodologies to precisely target, engage, and convert high-value cohorts, contact our team at marketing@yoyi.com.cn. Leveraging advanced DMP analytics and deep market intelligence, our consultants design bespoke strategies that align with your brand’s objectives, ensuring competitive differentiation and measurable ROI in China’s dynamic luxury sector.

Source of featured image: Photo by Laura Chouette on Unsplash